Your credit score is directly associated with your credit history. The credit score is the crucial factor in determining the state of the cardholder in procuring an external loan, opening a bank account, and getting suitable car insurance. These facilities can get eroded by a single mispayment of credit.

A credit score is something that plays a crucial factor. In case you are planning to obtain any loan, be it a home loan or a new credit card. Also, opening a simple bank account or finding car insurance, credit score plays a vital role.

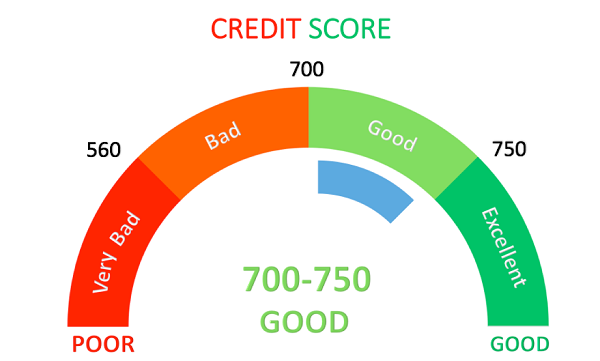

The regular payments of credit cards will give rise to advent events such as reducing your credit score and suppressing your credit history. A credit score helps in building a strong credit history, thus providing a reliable, creditworthy profile to the borrower or cardholder as per the situation implies. As per the terms of CIBIL, the range of credit score is between 300 to 900, where qualifying to 750 points lead you to faster approval of credit. Thus, it is essential to give a boost to your credit score to gain benefits in the financial market.

Factors affecting your credit score to worse

The importance of credit scores marks a material impact on your financial life. Higher credit scores provide a lower risk of default. In case of dropping of a credit score, one cannot decide why and how to fix those issues. Following are the factors negatively affecting your credit score:

Missing the due dates:

The adverse effect of losing your credit card bill and monthly installments exerts a negative impact on your credit history. The credit report reflects all the missed EMI history showing the number of days for which the bills remained unpaid. If the same condition persists, the negative mark may outlast in your credit history. On the other hand, if you start paying your bills on time, your credit history will improve within 6 to 8 months.

Frequently increasing your credit card limit:

A considerate increase in your credit card limit signifies dependency on credit in terms of managing expenses. This exhibits non-promising signs to the lenders.

Not having a credit history:

It might sound surprising to the fact of not having a credit history, either negative or positive, can even affect the credit score. Having no past credit cards, or have not taken any loan in the past puts a pause to your credit report. The absence of your credit history makes it difficult for the lenders to analyze the category which the borrower falls in.

Not maintaining a credit utilization ratio:

This implies the inability to maintain a desired credit utilization ratio provided by the credit card issuer. If the cardholder either over-utilized or underutilized the credit, it will disturb the credit utilization ratio, thereby damaging the credit scores.

You are under more than one debt:

Another significant reason for the credit score not improving is the state of the cardholder being under the liability to repay the old debts. A default on the previous loan gets reflected on the credit history based on which your credit score shall be analyzed. To improve one’s credit score, one must settle the existing credits and enjoy the benefits of credit score.

Your credit report has an error

The credit report is an essential document. Wrong information displayed can create many problems in the process of sanctioning of the loan.

For example, if you make your car payment regularly. But if it is reported late in the report, it can lead to an administrative error. It is essential to inform the credit bureaus and make the corrections.

A self-evaluation of the report is a must. Decimal in the wrong place can change your financial position. A misapplied name can lead to the interchange of the report of the two people.

Fault Detected

Though it is the rarest of the event possible, however, we need to invigilate all the factors. There might be some suspicious activities that are landed in your report. Keep a clear check on all your accounts. In the case of such an event, all the banks and lenders and credit bureaus are supposed to be informed about the same. Hiring a professional can also help to resolve the issue and fixing up your credit.

Your credit history is not diversified enough

Having diversification in your portfolio or a credit mix plays a vital role. A mix combination in the form of an installation account, revolving account, and open account can be a great combination.

Therefore, one must consider the above factors and avoid the situations arising negative impact on the credit score since a credit score is an integral part of the credit history, which can be the most beneficial for your financial assistance in the future.

Also, we can conclude that making prompt payment and clear your dues on time can help to increase your credit score. On the other hand, late payment can make your credit score worse.

3,010 total views, 9 views today